China’s Strategic Turn Toward Economic Autonomy: A Structural Shift the United States Must Understand

By Dr. Driss Effina

Over the past two decades, the dominant American narrative about China was built on a simple premise: China’s economic rise was inseparable from its deep integration into global markets. It was the world’s factory, dependent on Western consumers, foreign capital, imported technology, and global supply chains. That interpretation was not wrong in the early 2000s. But it is increasingly incomplete today.

A quiet structural shift is underway. China’s total trade (exports plus imports) as a share of GDP has fallen dramatically since its peak. In 2006, trade represented 63.57% of China’s GDP. By 2023, that figure had declined to 36.11%. This is not a marginal fluctuation; it is a macroeconomic transformation. Meanwhile, the United States’ trade-to-GDP ratio stands around 24–25%, reflecting the typical profile of a large continental economy with a massive domestic market and strong services base.

The implication is not that China is “closing off” or withdrawing from global commerce. In absolute terms, China remains one of the largest trading nations on earth. Rather, Beijing is recalibrating its exposure to the global system. The ratio is falling because China’s domestic economy is growing in size and complexity, because its internal supply chains are deepening, and because policymakers are deliberately reducing strategic vulnerabilities.

The key question for American policymakers is not whether China trades more or less. It is whether China is building an economic structure capable of sustaining growth even under geopolitical stress, technological containment, or partial decoupling. If so, that represents a shift in the balance of economic leverage.

From Hyper-Integration to Managed Exposure

In the early 2000s, China’s growth model was heavily export-driven. Its accession to the World Trade Organization in 2001 triggered a surge in exports. Foreign direct investment flowed in. China integrated deeply into global production networks. By 2006, the country’s trade-to-GDP ratio had reached nearly two-thirds of national output an extraordinary level for an economy of its size.

But that peak also revealed a vulnerability: reliance on external demand made China sensitive to global cycles. The 2008 financial crisis exposed this fragility. Beijing responded with massive domestic stimulus, infrastructure expansion, and investment-led growth. Over time, the policy narrative shifted from export-led expansion to domestic rebalancing.

The decline in the trade ratio since 2006 reflects this reorientation. China’s GDP expanded rapidly, services grew as a share of output, and domestic consumption gradually increased. Even though China’s exports remain enormous in absolute value, the economy is less dependent on them proportionally. The denominator GDP has grown faster than the numerator.

This evolution mirrors the structural path of other large economies. The United States, because of its vast internal market, has always exhibited a lower trade ratio. Services dominate American GDP, and services are less tradable than manufactured goods. As economies mature and urbanize, internal activity becomes more prominent relative to cross-border flows. Yet in China’s case, structural maturation is only part of the story. The shift is also strategic.

Strategic Autonomy in an Era of Geoeconomic Competition

Since 2018, geopolitical tensions between Washington and Beijing have intensified. Tariffs, investment restrictions, and especially export controls on advanced semiconductor technologies have introduced a new dimension: technological containment.

The U.S. Bureau of Industry and Security’s export controls on advanced chips and semiconductor manufacturing equipment, first issued in October 2022 and expanded in 2023, signaled that access to cutting-edge technology could be restricted for strategic reasons. From Beijing’s perspective, this changed the calculus. Dependence on foreign technology was no longer simply a matter of efficiency; it became a matter of national vulnerability.

China’s response has been to accelerate domestic capability building in key sectors: semiconductors, artificial intelligence hardware, electric vehicle batteries, renewable energy systems, industrial robotics, and critical minerals processing. This push is embedded in long-term planning frameworks that emphasize science and technology self-reliance as foundational for national development.

The objective is not autarky. China continues to trade, invest, and participate in global markets. But the aim is selective autonomy to ensure that critical nodes of economic power cannot be externally disabled.

This ambition explains why the falling trade ratio matters. An economy less exposed to external demand and foreign inputs is more resilient under stress. If exports account for a smaller share of GDP, a disruption in foreign markets becomes less destabilizing. If imports of strategic components are replaced by domestic production, sanctions lose effectiveness. In power politics, resilience is leverage.

Comparing Structural Exposure: China and the United States

It is important for American readers to contextualize this transformation.

The United States’ trade-to-GDP ratio of roughly 25% reflects a structurally large domestic economy. U.S. exports account for about 11% of GDP, imports roughly 14%. America’s growth is primarily internally driven. Consumer spending alone represents around 70% of GDP.

China’s current 36% trade ratio remains higher than America’s, but it is far lower than its 2006 peak. The direction of change suggests convergence toward the profile of a mature large economy. Yet the underlying motivation differs. The U.S. did not deliberately reduce trade dependence; its structure evolved naturally over decades. China, by contrast, is managing its exposure in response to geopolitical incentives.

The distinction matters. When a country intentionally reduces dependence, it is signaling preparation for a more contested global environment.

At the same time, the United States is also recalibrating. The CHIPS and Science Act allocates over $50 billion to rebuild domestic semiconductor capacity. The Inflation Reduction Act channels hundreds of billions into clean energy and industrial policy. Washington, too, is seeking to reduce strategic vulnerabilities in supply chains dominated by China.

Thus, we are witnessing a symmetrical adjustment. China reduces dependence on Western technology and demand. The U.S. reduces dependence on Chinese manufacturing and processing dominance. The global system is not collapsing; it is fragmenting along strategic lines.

Economic Logic Behind the Shift

The macroeconomic mechanics can be illustrated simply. GDP equals consumption plus investment plus government spending plus net exports. If domestic consumption and investment rise faster than trade flows, the trade-to-GDP ratio declines.

In China’s case, investment in infrastructure, urbanization, high-speed rail, digital networks, and renewable energy has expanded domestic activity. Services such as finance, e-commerce, logistics, and digital platforms have grown rapidly. These sectors are less directly tied to cross-border trade.

Simultaneously, import substitution policies increase domestic content in manufacturing. When domestic firms produce inputs previously imported, imports fall relative to GDP. The ratio declines even if final exports remain strong.

From a modeling perspective, trade openness can be understood as a function of service-sector share, domestic value-added content, exchange rate dynamics, and geopolitical shocks. The post-2018 environment introduced structural incentives to internalize supply chains.

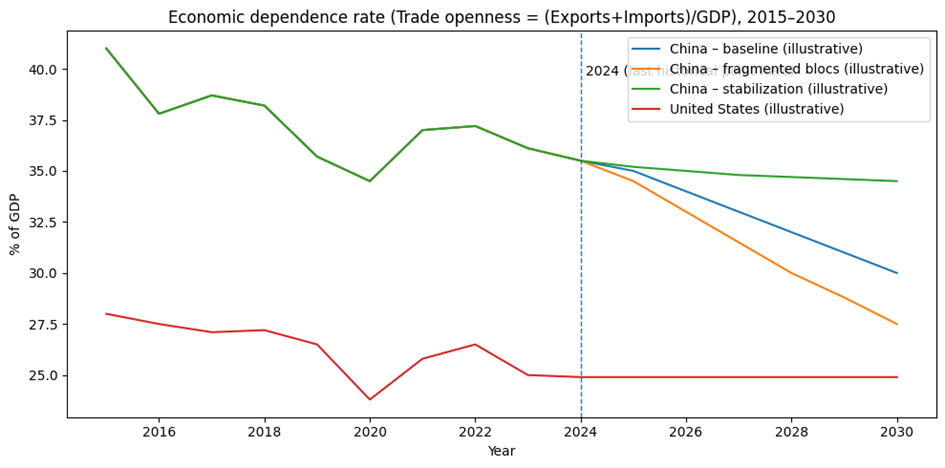

Three Scenarios for 2025–2035

Looking forward, three plausible scenarios emerge.

Scenario 1: Managed Interdependence

Under this scenario, both China and the United States continue strategic adjustments but avoid full decoupling. Trade remains substantial, though more diversified. Critical technologies are partially separated, but consumer goods and non-sensitive sectors remain integrated.

China’s trade-to-GDP ratio stabilizes around 30–35%. Domestic consumption expands gradually. The U.S. strengthens domestic manufacturing without severing ties with global markets. Global growth slows modestly due to redundancy costs, but systemic stability persists.

Scenario 2: Fragmented Tech Blocs

In this scenario, technology restrictions expand significantly. AI chips, advanced manufacturing tools, and critical materials become battlegrounds. Parallel supply chains and standards emerge. Trade ratios decline further for China and potentially for the U.S.

China’s openness could fall below 30% as domestic substitution accelerates. The U.S. and its allies consolidate supply chains within friendly networks. Duplication of capacity raises costs. Global inflationary pressures intensify due to reduced efficiency.

Strategic autonomy increases, but global productivity growth slows. The world divides into semi-distinct economic ecosystems.

Scenario 3: Strategic Stabilization

In this more optimistic scenario, both powers recognize the costs of fragmentation and negotiate limited frameworks for technology trade and supply chain coordination. Export controls remain targeted rather than expansive. Trade stabilizes.

China’s openness stabilizes around current levels. U.S.–China competition persists but within defined guardrails. Economic growth continues with moderated risk.

This scenario requires political restraint and mutual recognition of interdependence.

Implications for American Strategy

China’s declining trade share should not be interpreted as weakness. It reflects preparation for endurance. A less trade-dependent economy can better withstand sanctions, tariffs, and demand shocks. It can sustain industrial campaigns over longer horizons.

For the United States, the strategic question is not how to prevent China from trading. It is how to ensure that American resilience keeps pace. Overly aggressive containment may accelerate China’s autonomy drive. Insufficient domestic investment may increase American vulnerability.

The competition of the next decade will center on systems who controls standards, supply chains, platforms, and industrial ecosystems. Economic independence in this context means the ability to absorb disruption without systemic collapse.

Conclusion

China’s shift from a 63.57% trade-to-GDP ratio in 2006 to 36.11% in 2023 signals a profound structural transformation. It is not a retreat from globalization but a recalibration of exposure. Beijing is building an economy capable of sustaining growth even in a hostile geopolitical environment.

The United States must recognize this as a strategic signal. Economic autonomy selective, managed, and focused on critical nodes is becoming a defining feature of 21st-century great-power competition.

If China succeeds, it will enter the next decade not as a hyper-dependent exporter, but as a resilient industrial system with greater strategic leverage.

The decisive question for America is not whether China trades more or less. It is whether the United States can match resilience with resilience and shape a global order where competition does not slide into fragmentation beyond repair.

We are not witnessing the end of globalization. We are witnessing its strategic reconfiguration.